Frequently Asked Questions

Nri Banking

How NRI/PIO in the UK Can Earn Tax-Efficient Returns with FCNR(B) Deposits

Explore FCNR(B) deposits for UK NRIs to earn tax-free interest, avoid currency risk, and grow overseas savings confidently.

Synopsis

UK-based NRI/PIO can use FCNR(B) deposits to hold eligible savings in Pound Sterling and earn interest with tax benefits in India, subject to applicable laws.

FCNR(B) deposit may suit India-linked savings, while Cash ISAs can remain useful for UK tax-free savings.

Compare current HDFC Bank interest rates, deposit tenure and UK tax implications before booking.

Overview

For many NRIs living in the UK, saving decisions are not limited to a single country. You may earn and spend in pounds, build assets in the UK and still have future plans in India, such as supporting family, funding education, buying property or preparing for retirement.

That is where an FCNR(B) Fixed Deposit can become relevant. It allows eligible NRI/PIO to hold a fixed deposit in a supported foreign currency, including Pound Sterling, rather than converting the deposit into Indian Rupees.

The key point is simple: FCNR(B) deposit can be tax-efficient, but it is not automatically tax-free in every country. While the interest is generally exempt from tax in India for eligible customers, UK tax treatment depends on your UK residence status, income tax position and any available reliefs.

What “Tax-Efficient” Really Means for a UK-Resident NRI

For a UK-resident NRI, tax efficiency needs to be viewed across both India and the UK.

On the India side, FCNR(B) interest is generally exempt from income tax in India for eligible NRI/PIO. This can make it different from some India-linked deposits where tax may apply to interest income.

On the UK side, interest earned from an FCNR(B) deposit may be treated as foreign savings income. UK residents normally need to consider foreign income for UK tax purposes, even where the income is exempt in India.

This does not make FCNR B deposit less useful. It simply means the product should be assessed for the role it plays in your overall savings plan. For example, it may suit money you expect to use in India or money you want to retain in GBP while keeping an India banking connection.

Where FCNR(B) deposit Sits Among Your UK Options

FCNR(B) deposit is not a replacement for every UK savings product. It serves a different purpose.

| Option | Best suited for | Key consideration |

|---|---|---|

| Cash ISA | UK tax-free savings within the annual ISA limit | Interest is tax-free in the UK |

| Fixed-Rate Bond | UK savings where a fixed return and defined term are preferred | Interest may be taxable outside a tax wrapper |

| Premium Bonds | Savers comfortable with prize-based outcomes | Returns are not guaranteed |

| GBP FCNR(B) Deposit | India-linked savings held in Pound Sterling | Interest may be taxable in the UK |

A well-planned savings strategy may use more than one option. A Cash ISA can be useful for UK tax-free savings, while a GBP FCNR(B) deposit may be considered for eligible savings that are linked to India or intended to remain in foreign currency.

Versus a Cash ISA

A Cash ISA is designed for tax-free savings in the UK. For the 2026–27 tax year, the overall ISA allowance is £20,000, subject to eligibility and applicable rules.

FCNR(B) serves a different need. It is a foreign currency deposit for eligible NRIs and does not use up your ISA allowance. It can therefore be relevant when:

You have already used your ISA allowance

You want to hold funds in GBP rather than INR

Your future financial goals are linked to India

You prefer a fixed deposit structure for a chosen tenure

However, a Cash ISA has one clear advantage for UK tax purposes: interest earned within it is tax-free in the UK. Interest from an FCNR(B) deposit should be reviewed under UK tax rules.

Versus Fixed-Rate Bonds and Premium Bonds

A UK fixed-rate bond may offer a known return for a fixed period, usually in Pound Sterling. Depending on where it is held, the interest may be taxable in the UK.

Premium Bonds work differently. They do not pay regular interest. Instead, they provide an opportunity to win tax-free prizes through monthly draws. This can appeal to savers who want easy access and are comfortable with variable outcomes, but they do not provide guaranteed returns.

A GBP FCNR(B) deposit is different again. It offers a fixed-deposit route for eligible NRIs who want to retain savings in Pound Sterling while maintaining an India banking relationship. Principal and interest are fully repatriable, subject to applicable terms and regulations.

Understanding FCNR(B) deposit’s Tax Benefits in India

HDFC Bank FCNR(B) deposits offer eligible NRIs the benefit of tax-exempt interest in India. This can be useful for customers who want to build an India-linked corpus without creating additional Indian tax on the interest earned.

FCNR(B) deposits can be held for tenures ranging from one year to five years. The deposit is maintained in a foreign currency, helping reduce exposure to INR movement during the deposit period.

Tax treatment can depend on your residential status and applicable laws. If your residency status changes, particularly after a permanent return to India, it is important to review the account treatment with the Bank and a qualified tax adviser.

The UK Side: HMRC Treatment and the India–UK DTAA

For most UK-resident NRIs, FCNR(B) interest should not be viewed as automatically tax-free in the UK.

UK residents normally pay tax on foreign income, including foreign savings interest. Depending on your income tax band, your Personal Savings Allowance may cover a part of your total savings interest. Basic-rate taxpayers may receive up to £1,000 of savings interest at a 0% rate, while higher-rate taxpayers may receive up to £500. Additional-rate taxpayers do not receive a Personal Savings Allowance.

There is also a separate Foreign Income and Gains regime for certain qualifying new UK residents. This is not automatic and depends on specific conditions, including prior non-UK residence and a claim through the Self Assessment process.

The India–UK Double Taxation Avoidance Agreement helps address situations where the same income is taxed in both countries. However, it does not automatically make FCNR(B) interest tax-free in the UK. Where Indian tax is not payable on eligible FCNR(B) interest, there may be no Indian tax available for credit against a UK tax liability.

Consider advice from a UK-qualified tax professional before relying on any tax allowance, relief or treaty position.

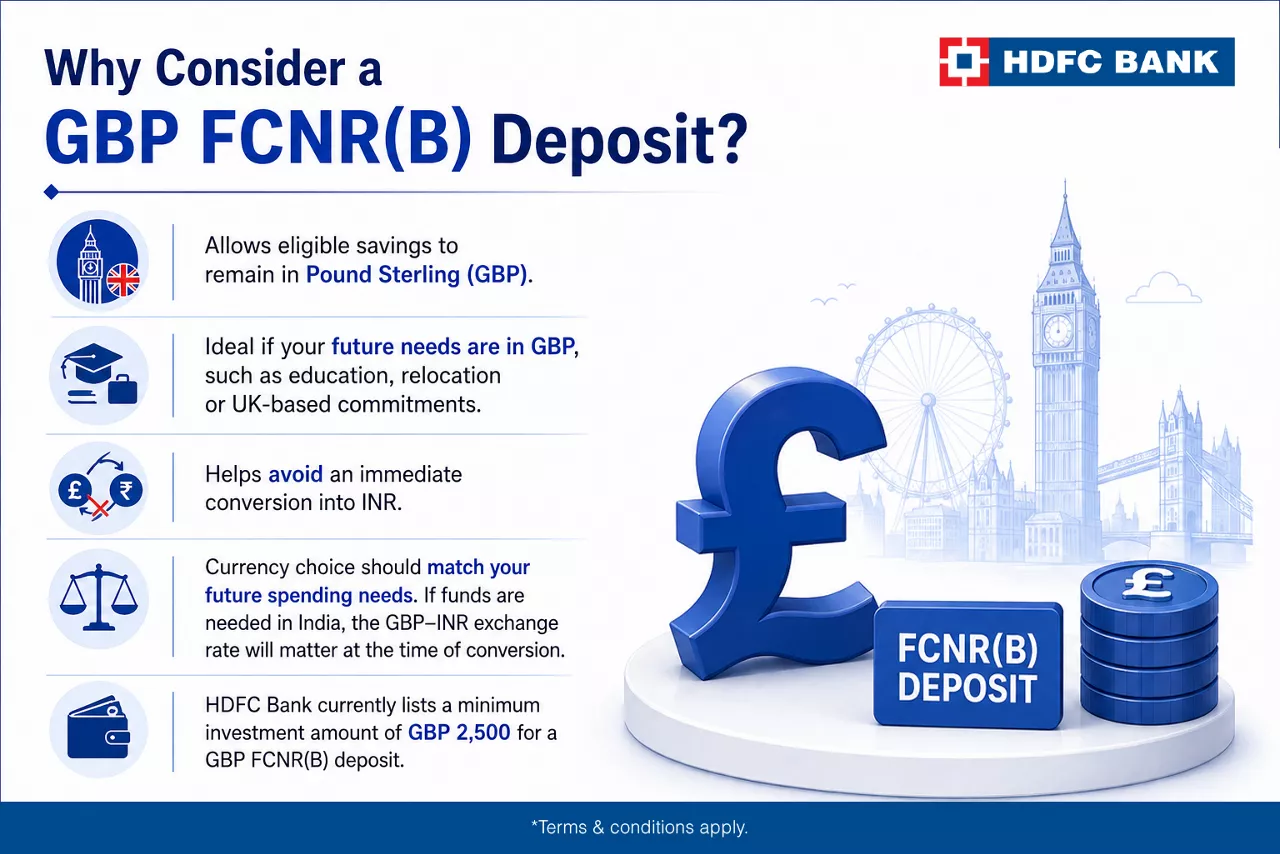

Why Consider a GBP FCNR(B) Deposit?

For NRIs living in the UK, the GBP FCNR(B) deposit can be relevant because it allows eligible savings to remain in Pound Sterling.

This may work well where your future needs are also in GBP, such as education expenses, relocation plans or UK-based financial commitments. Holding the deposit in GBP can help avoid an immediate conversion into INR.

At the same time, currency choice should be linked to your future spending needs. If you expect to use the funds in India in INR, the GBP–INR exchange rate at the time of conversion will still matter.

HDFC Bank currently lists a minimum investment amount of GBP 2,500 for a GBP FCNR(B) deposit. The applicable exchange rate, deposit rate and terms should be checked at the time of booking.

Timing It With the 2026 Rate Window

Interest rates on FCNR(B) deposits vary by currency and tenure. As per HDFC Bank’s interest rate effective 22 June 2026, the published GBP rate for tenures from three years to five years is 5.90% per annum. Rates are subject to change and the applicable rate is the one prevailing when the deposit is processed.

HDFC Bank also states that FCNR(B) deposits booked for three to five years between 10 June 2026 and 30 September 2026 carry a one-year lock-in period.

Before booking, compare:

The current GBP FCNR(B) rate

Your preferred tenure

Your expected need for the funds

UK tax treatment of the interest

Premature withdrawal conditions

No interest is payable if an FCNR(B) deposit is withdrawn before one year provided the deposit is not booked between 10 June 2026 and 30 September 2026. For withdrawals after one year, the applicable interest treatment is based on HDFC Bank’s prevailing terms.

View Current FCNR(B) Rates

Conclusion

For UK-based NRIs, FCNR(B) deposit can be a useful addition to a broader savings plan, especially when you want to retain eligible savings in Pound Sterling while keeping them connected to India.

The product’s Indian tax treatment, foreign currency holding and full repatriability can make it relevant for medium-term India-linked goals. But it should be evaluated alongside UK options such as Cash ISAs, fixed-rate bonds and Premium Bonds.

The most important step is to match the deposit currency, tenure and tax treatment with your own plans. Check the latest HDFC Bank rates and terms before booking, and obtain independent tax advice where required.

Disclaimer: Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Rates and terms are subject to change. Please refer to HDFC Bank’s official FCNR(B) rate card for the most current information.

If you are UK resident for tax purposes, you will normally need to consider FCNR(B) deposit interest as foreign savings income for UK tax purposes. Your final tax position may depend on your total income, Personal Savings Allowance and eligibility for any applicable relief.

Your Personal Savings Allowance can apply to eligible savings interest, including foreign savings interest, depending on your individual UK tax position. Basic-rate taxpayers may receive up to £1,000 and higher-rate taxpayers up to £500 of savings interest at a 0% rate. Additional-rate taxpayers do not receive a Personal Savings Allowance.

They serve different purposes. A Cash ISA offers UK tax-free savings within the annual ISA limit. FCNR(B) may be relevant for eligible NRI savings that are linked to India and held in a foreign currency such as GBP. The right option depends on your tax position, currency preference, tenure and financial goals.

The India–UK DTAA may help where the same income is taxed in both countries. However, FCNR(B) interest that is exempt from tax in India is not automatically exempt from UK tax. Consider professional tax advice for your individual position.

Yes. HDFC Bank offers FCNR(B) deposits in Pound Sterling, subject to eligibility and applicable terms. The current minimum amount for a GBP FCNR(B) deposit is GBP 2,500, subject to change.

Related Blogs

Make the most of your savings with our foreign

currency deposits