Frequently Asked Questions

Nri Banking

A Guide to FCNR(B) Deposits for NRIs Living in Dubai and the UAE

UAE-based NRIs can maximise tax-efficient foreign currency savings through FCNR(B) deposits, benefiting from higher rates, full repatriability and flexibility.

Synopsis

UAE-based NRIs can hold eligible savings in foreign currency through FCNR(B) deposits and earn tax-beneficial interest in India, subject to applicable laws.

The AED–USD link can make USD FCNR(B) deposits relevant for UAE-based savers.

Compare current HDFC Bank rates, tenure and withdrawal terms before booking.

Overview

If you live and work in the UAE, you already benefit from one of the world’s most tax efficient environments — no personal income tax. But many UAE-based NRIs don’t realise that the money they send back to India can be equally tax-efficient. FCNR(B) deposits offer interest income that is completely exempt from Indian income tax. Put the two together and you have a scenario that is genuinely rare: your savings work hard, and not a single rupee or dirham goes to tax on those returns. With RBI’s June 2026 changes pushing FCNR(B) rates to multi-year highs, this has never been a better time for UAE-based NRIs to take a closer look.

Why UAE-Based NRIs Are a Natural Fit for FCNR(B)

The AED-USD link makes currency choice simple. The UAE Dirham has been pegged to the US Dollar since 1997 at a fixed rate. This means that for a UAE-based NRI, opening a USD-denominated fcnr b deposit is effectively holding savings in the same currency your salary arrives in — there is no meaningful conversion risk at the source.

The double-zero tax advantage. UAE levies no personal income tax. India exempts FCNR(B) interest from income tax for NRIs. This combination means your returns from an FCNR(B) deposit are tax-free in both jurisdictions — a genuinely unusual position for any investment product.

No TDS deducted in India. Unlike NRO accounts where TDS is deducted at source, FCNR(B) interest is paid without any Indian tax deduction. You receive the full stated rate.

Remittance flows are already high. The UAE is consistently among the top sources of remittances to India. Many UAE-based NRIs are already moving money to India — an FCNR(B) deposit simply ensures that money is working at its highest potential rather than sitting in a low-yield account.

What RBI’s June 2026 window Mean for You

Effective June 17, 2026, RBI temporarily removed the interest rate ceiling on FCNR(B) deposits with 3-5 year tenors. Separately, since June 8, RBI has been running a special swap window that absorbs the currency hedging cost banks usually factor into FCNR(B) pricing — typically 3-3.5% annually.

The practical result: USD FCNR B rates have moved up meaningfully across banks, and HDFC Bank has revised its offerings in line with these changes. Both relaxations are scheduled to run until September 30, 2026.

What You Actually Earn Consider a UAE-based professional with USD 50,000 sitting in an overseas savings account earning [VERIFY: 1.5-2%]. The same amount in a 3-year USD FCNR(B) deposit at HDFC Bank, at the current elevated rates, earns significantly more — with no currency risk on the principal and no tax in India or the UAE. Check HDFC Bank’s current FCNR(B) rate card for the exact USD rate applicable to your tenor.

Full Repatriability — Your Money Can Always Come Back

A common concern for UAE-based NRIs is flexibility: what if I need the funds, or what if I decide to return to India or move elsewhere? FCNR(B) deposits are fully repatriable. Both principal and interest can be remitted back to your overseas account at any point after maturity, without restriction. There is no cap on the amount and no documentation hurdle for repatriation.

Who This Is For

This window is particularly relevant if you are:

A UAE-based Indian professional with foreign currency savings earning minimal returns in an overseas account

Planning to stay in the UAE for 3-5 more years and don’t need the funds immediately

Looking to build a tax-efficient corpus in India for future use — children’s education, property, retirement

Already sending money to an NRE account but not aware that FCNR(B) avoids the exchange-rate risk that NRE carries

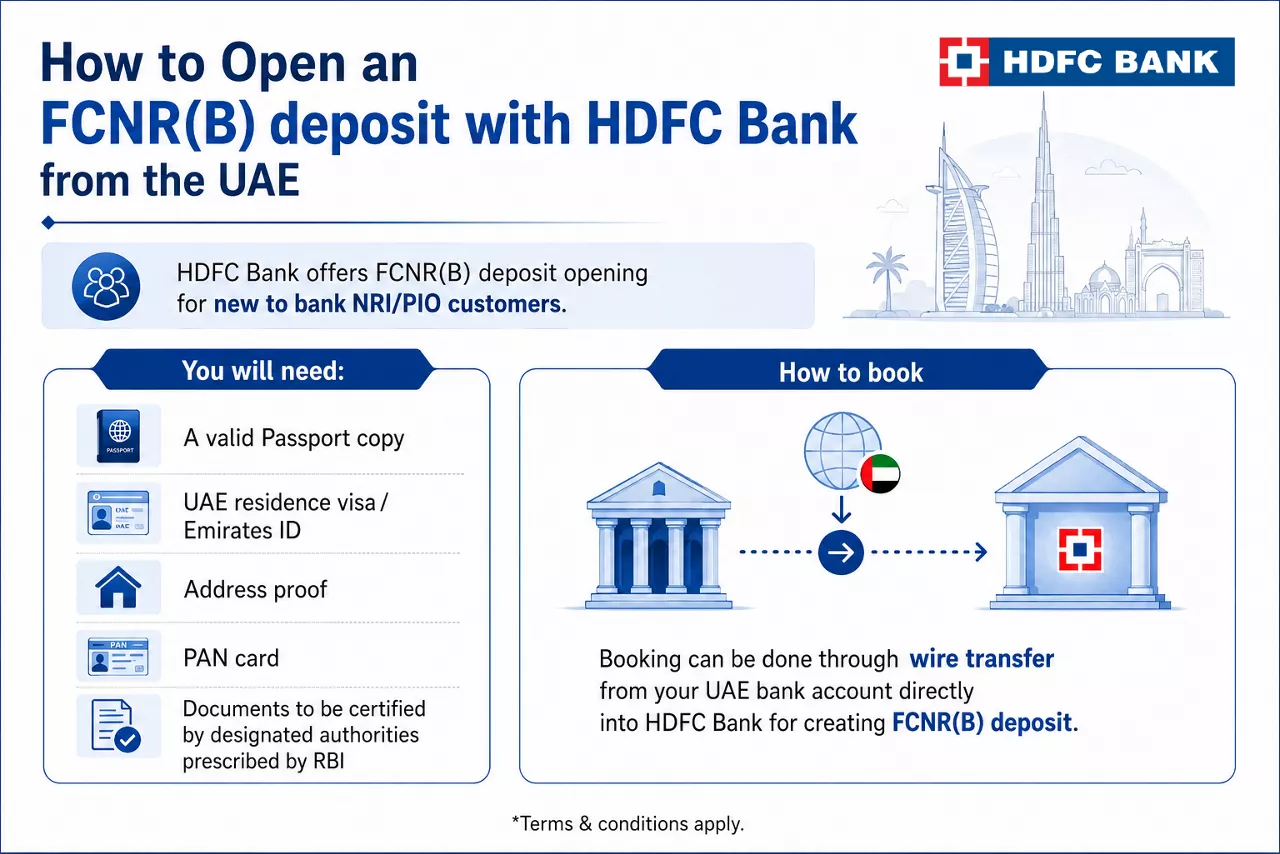

How to Open an FCNR(B) deposit with HDFC Bank from the UAE

HDFC Bank offers FCNR(B) deposit opening for new to bank NRI/PIO customers. You will need:

A valid Passport copy

UAE residence visa / Emirates ID

Address proof

PAN card

Documents to be certified by designated authorities prescribed by RBI

Booking can be done through wire transfer from your UAE bank account directly into HDFC Bank for creating FCNR(B) deposit.

Check HDFC Bank’s current FCNR(B) rates for UAE-based NRIs and open your account online

*Disclaimer: Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Rates and terms are subject to change. Please refer to HDFC Bank’s official FCNR(B) rate card for the most current information.

Yes. UAE has no personal income tax. India exempts FCNR(B) interest income for NRIs. No tax applies in either country on the interest earned.

FCNR(B) deposits accept supported foreign currencies. USD is the most common choice for UAE-based NRIs given the AED-USD peg. Check HDFC Bank’s supported currency list.

Minimum deposit thresholds vary by bank and currency. Check HDFC Bank’s FCNR(B) deposit terms for the applicable minimum amount.

Yes. HDFC Bank supports online deposit booking through netbanking for existing customers and non-face to face account opening cum deposit booking for new to bank NRI/PIO customers. Documentation for non-face to face NR account opening can be submitted via courier provided are additionally certified by designated authorities prescribed by RBI.

If your residential status changes to Resident Indian, FCNR(B) deposit will continue till maturity. Interest earned from said deposit needs to be reported by customers independently to Indian income tax authorities and pay the applicable taxes since bank will not deduct TDS from their end. Discuss with your HDFC Bank relationship manager when this happens.

Related Blogs

Make the most of your savings with our foreign

currency deposits