Frequently Asked Questions

Nri Banking

FCNR(B) Rates Just Got a Major Boost: Know How to Lock In

Foreign Currency Non-Resident (FCNR) (B) deposit rates have increased after RBI’s 2026 rate relaxatoin during swap window. Here’s how NRIs can lock in higher returns in foreign currency with HDFC Bank before the window closes.

Synopsis

Two RBI moves in June 2026 – the rate relaxation and the hedging cost absorption – caused the FCNR (B) deposit rates to rise.

Foreign currency parked in an FCNR(B) deposit today could earn more than would have earned a few weeks ago.

Both RBI relaxations are scheduled to lapse on September 30, 2026.

Overview

For years, FCNR(B) deposits were the safe, steady and slightly unexciting option for NRIs parking foreign currency in India. However, that may have changed. Following two back-to-back RBI moves in June 2026, FCNR(B) returns are climbing toward levels not seen in years, and the window to lock in these rates has a hard deadline. Here’s what’s driving the surge, and why acting sooner rather than later matters.

Two RBI Moves, One Big Opportunity

Move 1: The rate relaxation.

On June 17, 2026, RBI temporarily relaxed the interest rate on FCNR(B) deposits with 3-5 year tenors, giving banks room to price deposits far more competitively, through September 30, 2026.

Move 2: RBI is footing the hedging bill.

Separately, RBI opened a special swap window on June 8, 2026, under which it absorbs the currency hedging cost — typically 3-3.5% annually — that banks usually pass on to depositors through lower rates. With that cost off the table, banks can offer materially higher returns on the same deposit.

Put together, these two moves remove the two biggest constraints that kept FCNR(B) rates muted.

The result: several banks have already begun revising interest rates upward, some sharply.

What “Higher Rates” Looks Like in Practice

Before these changes, 3-5 year USD FCNR(B) deposits typically yielded around 3-4% approx. Post-relaxation, banks have room to price well above that — and early movers in the market have pushed FCNR(B) interest rates considerably higher within days of the announcement.

The takeaway: foreign currency parked in an FCNR(B) deposit today could earn meaningfully more than what would have earned a few weeks ago with zero added currency risk, since FCNR(B) deposits stay in the foreign currency throughout the tenor.

Why the Timing Matters

Note that this isn’t an open-ended rate hike. Both RBI relaxations —are scheduled to lapse on September 30, 2026, unless RBI decides to extend them. Deposits booked within this window lock in their interest rate for the full tenor. However, uncertainty about the rates after September 30, 2026 persists.

If you’ve been sitting on foreign currency savings deciding when to move, this window is the kind of opportunity that may not come around often — RBI last ran a comparable window in 2013.

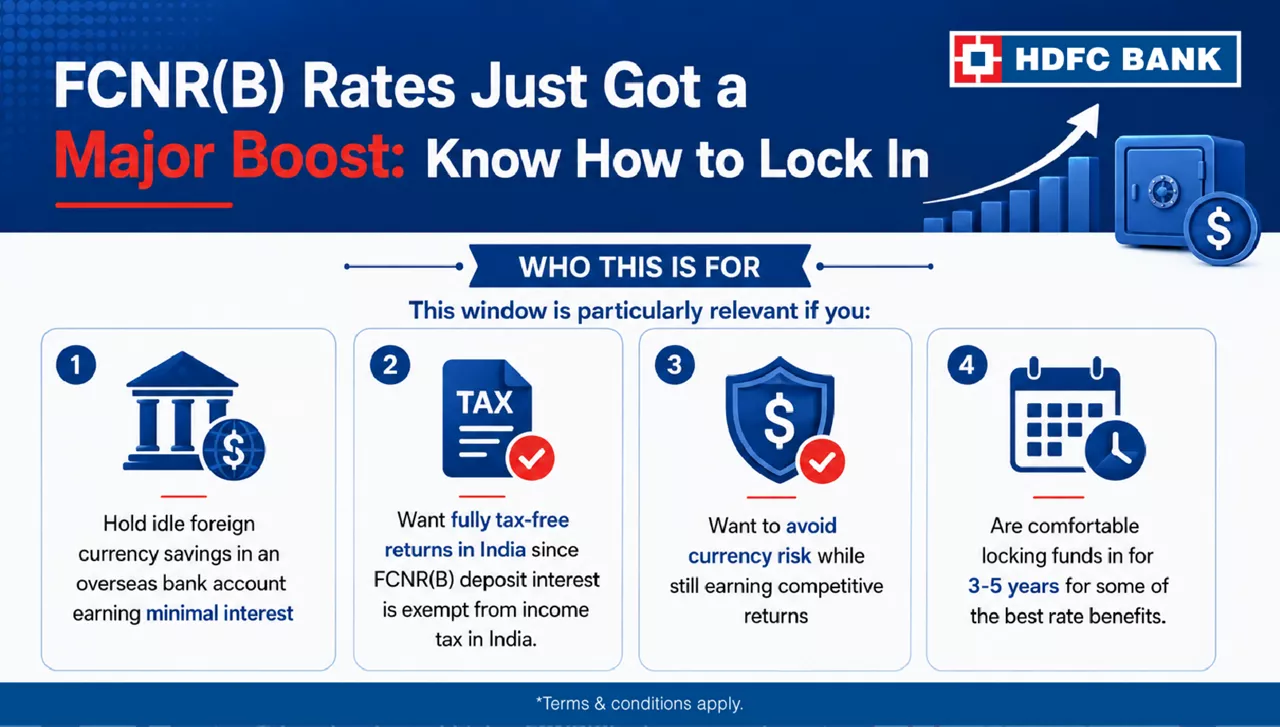

Who This Is For

This window is particularly relevant if you:

- Hold idle foreign currency savings in an overseas bank account earning minimal interest

- Want fully tax-free returns in India since FCNR(B) deposit interest is exempt from income tax in India.

- Want to avoid currency risk while still earning competitive returns

- Are comfortable locking funds in for 3-5 years for some of the best rate benefits. (Mandatory lockin of FD principal will be only for 1 year.)

Final Note: Lock In Your Rate with HDFC Bank

- Check HDFC Bank’s current FCNR(B) interest rate for your currency and tenor.

- Incase you don’t have an account with HDFC Bank yet then keep your NRI documentation ready — passport, address proof, Proof of NRI/PIO status, PAN/Form 97, declaration, etc.

- Open your account online or through your HDFC Bank relationship manager.

- Open the deposit via remittance, existing NRE balance, or FCNR(B) transfer.

- Lock in your interest rate for the full tenor before the relaxation window loses.

View HDFC Bank’s latest FCNR(B) deposit interest rates and open your NR account today

*Disclaimer: Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Rates and terms are subject to change. Please refer to HDFC Bank’s official FCNR(B) rate card for the most current information.

Once booked, your FCNR(B) deposit carries its interest rate for the entire tenor (1-5 years).

Interest rates may revert to standard RBI-determined ceilings unless the relaxation is extended. There’s no guarantee the current pricing will still be available after that date.

Minimum deposit amounts vary from currency to currency. You can check HDFC Bank’s FCNR(B) deposit features, benefits, terms and conditions for more details.

Note that premature withdrawal of FCNR(B) deposits booked during RBI swap window in HDFC Bank is permitted only after 1 year lockin without any penalty but typically attracts a lower applicable interest rate. FCNR(B) deposit is best suited for funds you won’t need before maturity.

Related Blogs

Make the most of your savings with our foreign

currency deposits