Frequently Asked Questions

Nri Banking

FCNR(B) Deposit Rate Window 2026: Should NRIs Act Now?

Understand the FCNR(B) deposit rate window, key RBI measures and factors to consider before September 30, 2026.

Synopsis:

- RBI’s temporary rate flexibility may support competitive FCNR(B) deposit rates until September 30, 2026.

- FCNR(B) deposits helps NRIs hold deposits in foreign currency while reducing INR exchange-rate exposure.

- Compare rates, tenure and liquidity needs before booking your deposit.

Overview

If you are an NRI with foreign currency savings, September 30, 2026 is an important date to keep in mind. The RBI’s relaxed rules on FCNR(B) deposits — the higher interest rate ceiling and the hedging-cost swap window — both have the same expiry date i.e. September 30, 2026. If you’ve been considering an FCNR(B) deposit, that date matters more than it might seem. Here’s what’s actually at stake, and how to think through the decision.

HDFC Bank is currently offering higher FCNR (B) deposit rates for NRI/PIO until September 30, 2026. The limited-period opportunity is linked to RBI’s temporary measures for FCNR(B) deposits, including relaxation in the interest rate ceiling and the hedging-cost swap window.

For customers, the key question is simple: should you book an FCNR(B) deposit during this swap window period or wait?

The answer depends on your currency, preferred tenure, liquidity needs and the prevailing FCNR(B) deposit rate available on the day your funds are received by bank.

What Is FCNR (B) Deposit?

FCNR(B), or Foreign Currency Non-Resident (B) Deposit, is a fixed deposit designed for NRI/PIO. It allows you to keep funds in eligible foreign currencies such as USD, GBP, EUR, AUD, SGD, JPY and CAD, instead of converting them into Indian Rupees (INR).

Since the deposit is maintained in foreign currency, the principal and interest are protected from INR exchange-rate movements. HDFC Bank also states that FCNR (B) deposit offer tax-free interest in foreign currency and full repatriability of principal and interest, subject to applicable regulations.

What Is Changing Until September 30, 2026?

Two RBI-linked measures are relevant for eligible FCNR(B) deposits during this period.

1. Temporary Relaxation in the Interest Rate Ceiling

Normally, FCNR(B) deposit rates are governed by RBI-prescribed interest rate ceilings linked to benchmark swap rates and applicable margins.

For the limited period, RBI has provided flexibility on the interest rate ceiling for specified FCNR(B) Deposit tenures. This gives banks greater flexibility to offer higher interestrates on said deposits.

In simple terms, this temporary relaxation may help customers get higher FCNR(B) interest rates than would otherwise be available under the regular ceiling-based framework.

2. Hedging-Cost Swap Window

The hedging-cost swap window is another RBI support measure linked to eligible FCNR(B) deposits.

Banks typically manage foreign currency exposure through hedging arrangements. Hedging has a cost, which can affect the rate a bank is able to offer on foreign currency deposits.

Under the special swap window, RBI support can help reduce the hedging cost borne by banks for eligible deposits. This may allow banks to offer more competitive FCNR(B) deposit rates during the applicable period.

For NRI/PIO customers, the practical takeaway is that the current interest rate environment is more attractive for FCNR(B) deposit of tenure between 3 – 5 years until September 30, 2026.

Why Does the Deadline Matter?

The current higher interest rate opportunity is time-bound.

HDFC Bank highlights that higher FCNR deposit rates are available until September 30, 2026. The exact rate you receive will depend on the currency selected, deposit tenure and the date on which clear funds are received by the Bank.

After September 30, 2026, RBI may extend, modify or discontinue the temporary measures. There is no assurance that the same rate environment will continue after the deadline.

This does not mean rates will necessarily fall. However, customers who want certainty on the prevailing FCNR(B) deposit interest rate may prefer to complete their booking within the available RBI swap window period.

Should You Book an FCNR(B) Deposit Now?

Consider an FCNR(B) deposit during this period if:

You have foreign currency which is earning low returns overseas.

You can keep the funds invested for the chosen tenor of 3 years to 5 years.

You want to avoid converting foreign currency into INR.

You are comfortable locking the funds for a fixed period of 1 year.

You have compared the prevailing FCNR(B) deposit interest rate with your overseas bank account or other NRI deposit options.

For example, HDFC Bank’s published FCNR rate card shows different rates based on currency and tenor. As of the listed effective dates, USD FCNR deposits for tenures between 3 years and less than 5 years show a rate of 6.00% p.a., subject to change.

When FCNR(B) Deposit May Not Be Suitable

An FCNR(B) deposit may not be suitable if:

You may need the money before 1 year .

You are likely to require frequent access to the funds.

You have not compared the current rate across currencies and tenures.

You are unsure whether FCNR(B), NRE Fixed Deposit or another investment option matches your financial goal.

Premature withdrawal may be permitted only after the lockin period of 1 year is completed subject to applicable terms, including reduced interest. Always review the latest terms before booking.

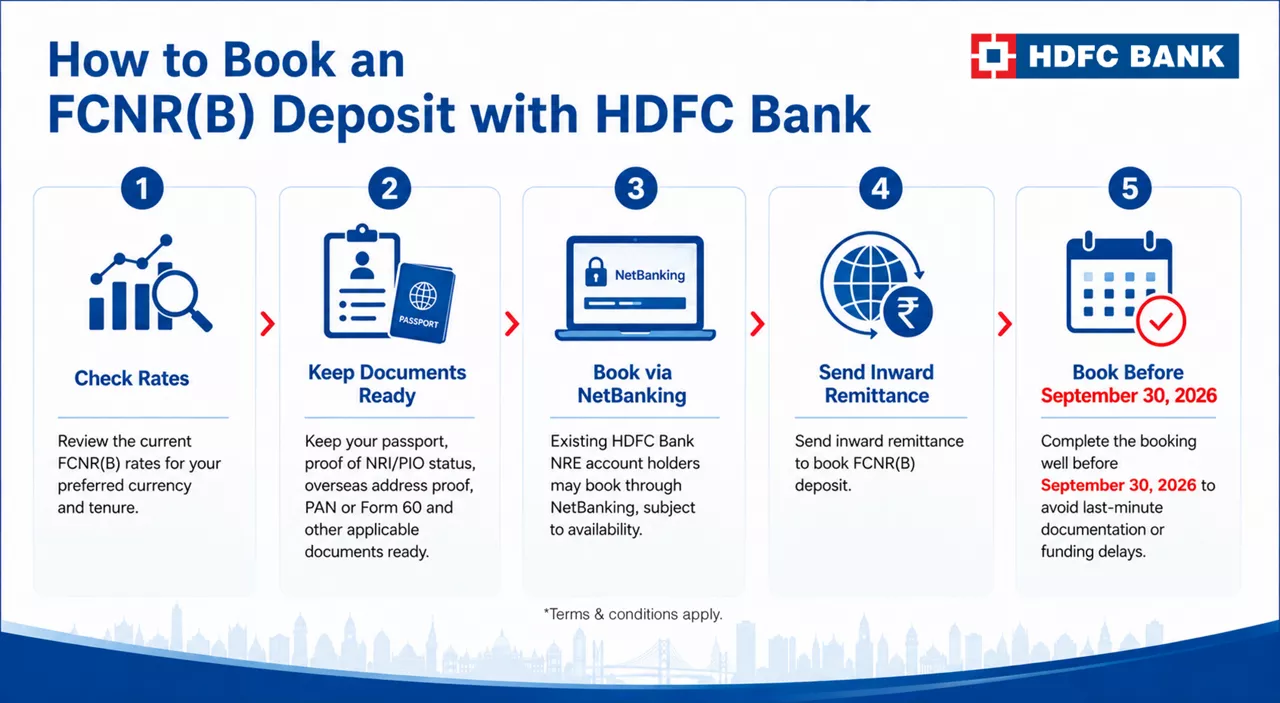

How to Book an FCNR(B) Deposit with HDFC Bank

- Review the current FCNR(B) rates for your preferred currency and tenure.

- Incase you do not have an account with HDFC Bank yet then kindly keep your passport, proof of NRI/PIO status, overseas address proof, PAN or Form 60 and other applicable documents ready.

- Existing HDFC Bank NRE account holders may book through NetBanking, subject to availability.

- Send inward remittance to book FCNR(B) deposit.

- Complete the booking well before September 30, 2026 to avoid last-minute documentation or funding delays.

HDFC Bank also provides guidance to NRI/PIO customers on How they can send remittances to India from abroad and for new NRI/PIO customers on How they can book FCNR (B) deposit through our various support channels.

Before You Decide

Do not select an FCNR(B) deposit only because of the deadline.

Check:

Currency-wise interest rate

Deposit tenure

Premature withdrawal terms

Funding method

Repatriation requirements

Your near-term liquidity needs

A deposit booked at the prevailing rate generally retains that rate for the selected tenure, subject to the applicable terms at the time of booking.

Conclusion

The September 30, 2026 FCNR(B) window is relevant for NRIs who want to lock in a prevailing foreign currency deposit rate for a planned tenure.

The temporary interest rate ceiling relaxation and hedging-cost swap window may support more competitive FCNR(B) deposit interest rates during the period. However, the right decision depends on your currency, return expectations, liquidity needs and investment horizon.

Explore HDFC Bank FCNR(B) Deposit rates and book your deposit before September 30, 2026.

*Disclaimer: Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Rates and terms are subject to change. Please refer to HDFC Bank’s official FCNR(B) rate card for the most current information.

HDFC Bank states that FCNR (B) deposit interest is tax-free in India for NRI/PIO.

It is an RBI support mechanism that can help banks manage currency hedging costs for eligible FCNR(B) deposits.

HDFC Bank states that higher FCNR deposit rates under RBI Swap window period are available until September 30, 2026.

Yes, customers may hold multiple FCNR(B) deposits, subject to applicable bank and regulatory rules.

Not necessarily. RBI may extend, modify or discontinue the temporary measures. Customers should check the prevailing HDFC Bank rate card before booking.

It is a temporary RBI-linked flexibility that allows banks greater scope to offer competitive rates on specified FCNR(B) deposits.

Related Blogs

Make the most of your savings with our foreign

currency deposits