Get Personal Loan up to ₹50 lakh with low interest rate

Loans

How to Improve CIBIL Score Immediately?

A high score can get you better and quicker loans.

Synopsis:

- Importance of a Good CIBIL Score: A high CIBIL score is crucial for obtaining better and quicker loans, while a low score can negatively affect borrowing capabilities.

- Ways to Improve CIBIL Score: Improve your score by paying dues on time, avoiding excessive debt, maintaining a balanced credit mix, applying for credit within limits, monitoring joint accounts, reviewing credit reports regularly, and gradually building a positive credit history.

- Role of CIBIL in India: CIBIL is a key credit rating agency in India, and banks use its scores to evaluate creditworthiness, with a score of 700+ considered excellent.

Overview

It pays to have a good credit score. A high score can get you better and quicker loans. However, a low CIBIL score can be terrifying for those individuals who have an urgent need for money; this can affect their borrowings adversely.

There are many ways to get loans, the criteria of which is totally grounded on the size of the loan, that is the amount required by the borrower. However, today all banks are compulsorily required to verify the CIBIL score of applicants of all financial products of credit, namely personal loans, credit cards etc. Even though at times the individuals may have a low CIBIL score, there are ways to improve CIBIL score.

In India, CIBIL is one of the leading credit rating agencies. Banks and financial institutions use the CIBIL credit score as a reference point to evaluate the credit-worthiness of borrowers. A score of 700+ is considered excellent. Anything lower than that and you will face problems getting loans quickly.

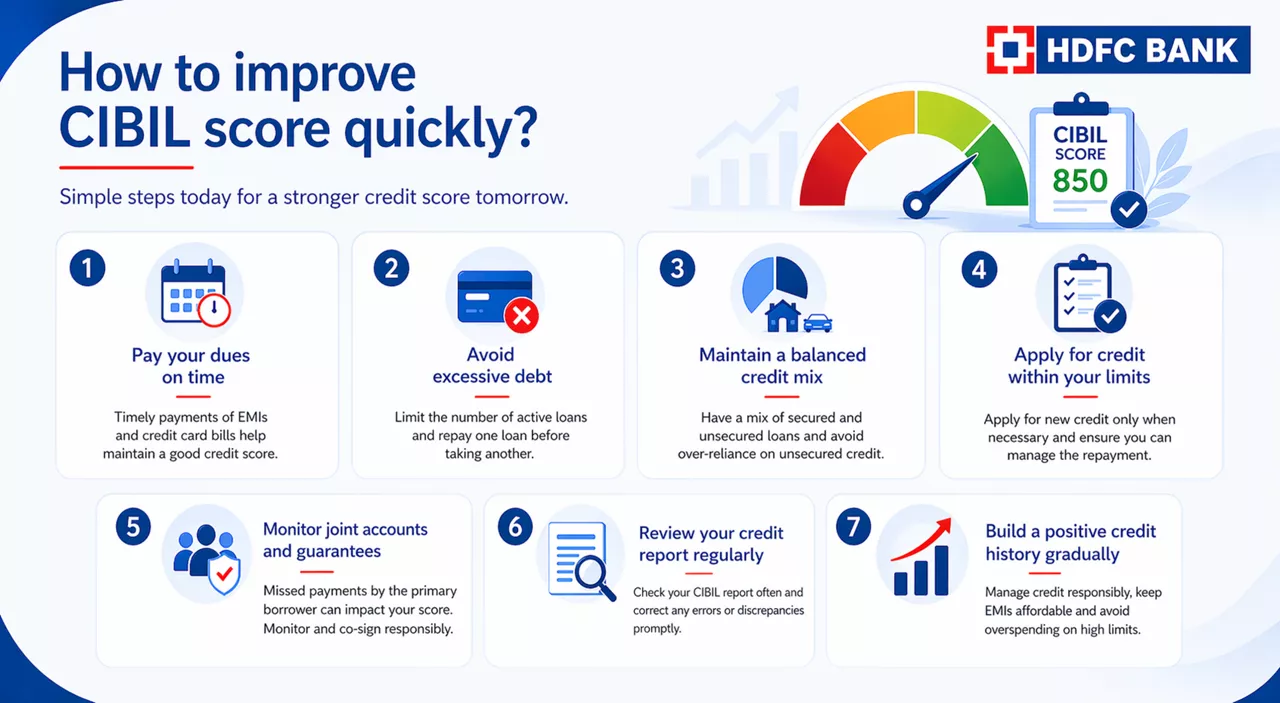

How to improve CIBIL score quickly?

All is not lost, though. You can build up your credit score with these seven smart moves. However, you need to practise these moves regularly and keep a tab on your Personal Loan EMIs and Credit Card monthly payments.

In India, CIBIL (Credit Information Bureau (India) Limited) is a prominent credit rating agency. Banks and financial institutions rely on CIBIL scores to assess borrowers' creditworthiness. A score of 700 or above is considered excellent, while a lower score can result in difficulties obtaining loans. Here’s how you can improve your CIBIL score swiftly:

1. Pay your dues on time

Timely payment of your EMIs and credit card bills is fundamental to maintaining a good credit score. Delays or missed payments can significantly lower your score. Set up reminders or automate your bill payments to ensure you never miss a deadline. Consistently paying your dues on time will positively impact your credit score.

2. Avoid excessive debt

Applying for multiple loans simultaneously can harm your credit score. It’s essential to use credit judiciously and limit the number of active loans. Focus on repaying a loan before taking on another. This approach demonstrates responsible borrowing behaviour and helps maintain a healthy credit score.

3. Maintain a balanced credit mix

Having a diverse mix of credit, including both secured (e.g., home loans, auto loans) and unsecured loans (e.g., personal loans, credit cards), is beneficial. A well-managed credit mix indicates to lenders that you can handle different types of credit effectively. Avoid excessive reliance on unsecured loans, as they may negatively impact your credit score.

If you are ready to borrow, you can Apply For Personal Loan online in just a few clicks.

4. Apply for credit within your limits

Only apply for new credit when necessary and ensure you can manage the repayment. Frequent credit applications may suggest financial instability, which can lower your score. Responsible credit use and only applying for credit you can afford will positively affect your CIBIL score.

5. Monitor joint accounts and guarantees

If you are a co-signer or guarantor on any loans, you share responsibility for the repayment. Any missed payments by the primary borrower can affect your credit score. Regularly monitor these accounts and avoid becoming a co-signer or guarantor unless necessary.

6. Review your credit report regularly

Check your CIBIL report frequently to identify and correct any discrepancies. Errors in your credit report, such as outdated information or incorrect entries, can negatively impact your score. Address any inaccuracies promptly to ensure your credit report reflects your true creditworthiness.

7. Build a positive credit history gradually

Building a good credit history takes time. Opt for a longer loan tenure if it results in lower EMIs and avoid overspending on high credit limits. Managing a higher credit limit responsibly, without increasing your expenditure, can positively influence your credit score.

Over time, you can build up a healthy score that can get you quick and competitive loans.

Read more about how to interpret your credit score.

* The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. All information is subject to the relevant