Get Personal Loan up to ₹50 lakh with low interest rate

Loans

How to check your CIBIL score online?

Understand the meaning of CIBIL score and learn the steps to check your score online.

Synopsis:

A CIBIL score reflects creditworthiness based on borrowing and repayment patterns.

Access your CIBIL score online by visiting the official website, registering, verifying identity, and reviewing your score.

Scores from 750-900 are excellent, 700-749 are good, 650-699 are average, and below 650 are poor, affecting loan terms and approvals.

What is a CIBIL Score?

A Credit Information Bureau (India) Limited (CIBIL) score is a three-digit number ranging from 300 to 900, calculated based on your credit history. It is a crucial aspect of your financial health, as it reflects your creditworthiness and plays a significant role in loan approvals and credit card applications.

CIBIL score is derived from the information provided by credit institutions about your borrowing and repayment patterns. A higher CIBIL score indicates better creditworthiness, which can improve your chances of getting approved for loans and credit cards.

Why Check Your CIBIL Score?

Regularly monitoring your CIBIL score can help you:

- Identify Errors: Spot inaccuracies or discrepancies that might affect your creditworthiness.

- Improve Credit Health: Take corrective measures if your score is lower than desired.

- Enhance Financial Planning: Plan for future credit needs and negotiate better terms on loans.

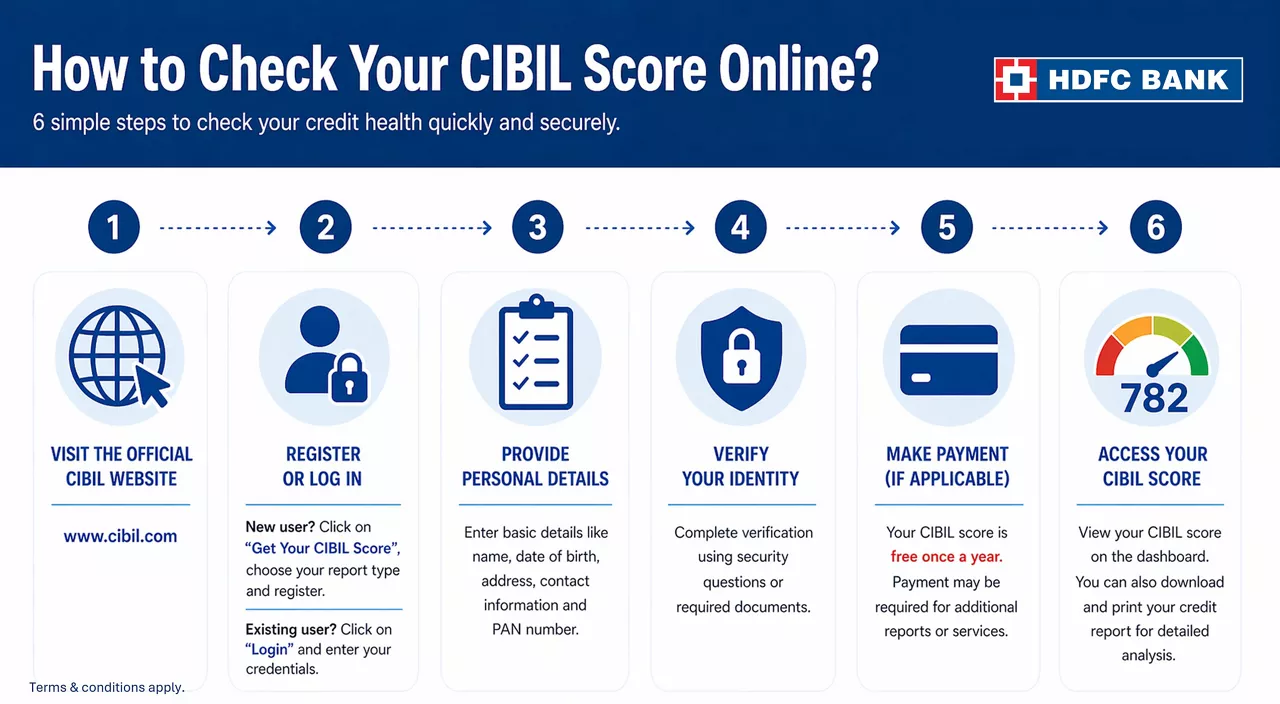

Steps to Check Your CIBIL Score Online

Follow the step below to check your CIBIL score online:

- Visit the Official CIBIL Website

To start, visit the official CIBIL website. Ensure you are on the genuine site to protect your personal information.

- Register or Log In

If you are a new user:

- Click on the “Get Your CIBIL Score” button.

- Choose the type of report you want (e.g., CIBIL Score & Report).

If you are an existing user:

- Click on the “Login” button.

- Enter your credentials to access your account.

- Provide Personal Details

You will need to provide the following details:

- Full Name: As per official documents.

- Date of Birth: To verify your identity.

- Address: For correspondence.

- Contact Information: Mobile number and email address.

- PAN Card Number: This is used for identity verification.

- Verify Your Identity

You may be asked to answer a few security questions or provide identification documents, to ensure the security of your information. This process helps prevent unauthorised access to your credit report.

Make Payment (if applicable)

While CIBIL often provides free access to your score once a year, there may be fees for additional reports or services. Review the payment options and make the necessary payment if required.- Access Your CIBIL Score

After completing the registration and verification process, you will be able to view your CIBIL score on the dashboard. You can also download and print your credit report for detailed analysis.

Interpreting Your CIBIL Score

Excellent (750-900)

A score in this range reflects a strong credit history. You are likely to receive favourable terms on loans and credit cards.

Good (700-749)

A good score indicates that you have a positive credit history. While you may still get loans and credit cards, terms might not be as favourable as those offered to individuals with an excellent score.

Average (650-699)

An average score suggests that there might be some issues in your credit history. You may face higher interest rates or stricter terms from lenders.

Poor (Below 650)

A score below 650 indicates a poor credit history. You might find it challenging to get credit approvals and may face higher interest rates.

Tips to Improve Your CIBIL Score

- Pay Bills on Time: Timely payment of credit card bills and loan EMIs positively impacts your score.

- Maintain Low Credit Utilisation: Use a small percentage of your available credit limit.

- Check for Errors: Regularly review your credit report for inaccuracies and dispute any errors.

- Limit Credit Inquiries: Avoid frequent applications for new credit as they can negatively impact your score.

Final Note

Checking your CIBIL score regularly helps you stay aware of your credit health and improve your chances of getting loans and credit cards. A good CIBIL score reflects responsible financial behaviour and can make borrowing easier in the future. Paying your dues on time, maintaining low credit utilisation, and monitoring your credit report for errors, helps you build and maintain a healthy credit profile.

*Disclaimer: Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances.